Are you planning to retire early? If so, you might be curious about how to budget your income and plan your expenses. Early retirees can face inflation. Social Security is another potential wild card. Fortunately, there are several strategies to help you plan your money well. Find out how to get started on your financial future. Here are some examples of strategies.

Saving for your early retirement

Budgeting for early retirement means putting aside money for certain expenses that you may not have thought of before. Most people budget for basic necessities like food and transportation, but it is important to include fun expenses such as travel. Moreover, you must also include the costs of purchasing a car. You will still need to pay for food, even though your income will be lower after retirement. You may be interested in learning to cook and entertaining friends.

It is also a smart idea to invest some of your income. As a general rule, you should invest at least 15% of your income towards your retirement. There may be an early withdrawal fee, however you can withdraw money that is in your retirement accounts before you turn 59 1/2.

Managing income streams

You need to identify, capture, and manage the income streams you have for early retirement. Social security benefits and pensions will most likely be your mainstay in retirement income. However, you should also consider other sources. These include real estate investments, dividends, and required minimum distributions.

It is important to identify the best investments that will yield the highest returns when managing income streams in early retirement. While the income from a lifetime annuity may be the most predictable, it is also subject to fluctuations due to inflation. It is crucial to take regular, strategic withdrawals that are based on your cash flow needs. Another method of creating a stable income stream is to invest in a CD ladder or bond ladder. Annuities that convert a lump sum to an ongoing income stream are a low-risk investment. You don't have to worry about falling stock prices or falling interest rate.

Financial enemy: Inflation

Inflation is an important aspect of planning for early retirement. This financial enemy can take away the purchasing power of your savings, and can threaten your financial security. Many retirees are living on fixed incomes and are therefore especially vulnerable to the impact of inflation. There are several ways that you can reduce the impact inflation has on your savings. You can protect your nest egg from inflation by managing your spending and investing.

Early retirees should invest in various forms of equities and income producing real estate to offset the effects of inflation. If they don’t have a retirement plan provided by their employer they should design one. The key advantage of this option is that the earnings and investment gains are not taxed. Moreover, early retirees should focus on building their own portfolio rather than relying on pensions or fixed annuities.

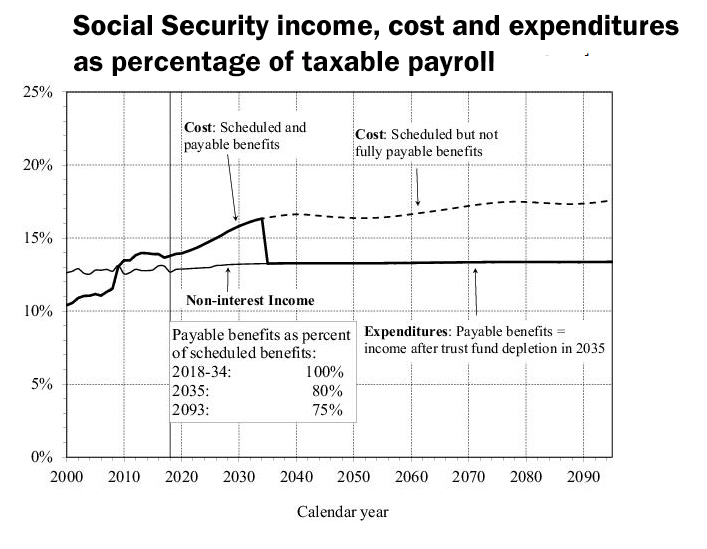

Social Security as a Wildcard for Early Retirees

Social Security Administration, or SSA, uses the "Retirement Earnings test" to determine if a beneficiary has enough time to receive all their benefits before they retire. This test allows SSA withhold benefits from beneficiaries that claim early. To avoid this wild card, you should save more for retirement.

Many early retirees are tempted to get their benefits earlier, particularly for those who were affected by Great Recession. The Center for Retirement Research at Boston College recently found that only 5% eligible people received their checks before full retirement age. You can fix funding problems by spending less money now and delaying retiring until you reach full retirement age, even if the system isn't funding your retirement as you expected.

FAQ

What are the benefits to wealth management?

Wealth management offers the advantage that you can access financial services at any hour. Savings for the future don't have a time limit. This is also sensible if you plan to save money in case of an emergency.

There are many ways you can put your savings to work for your best interests.

For instance, you could invest your money into shares or bonds to earn interest. To increase your income, you could purchase property.

If you use a wealth manger, someone else will look after your money. This means you won't have to worry about ensuring your investments are safe.

What is risk management and investment management?

Risk Management refers to managing risks by assessing potential losses and taking appropriate measures to minimize those losses. It involves identifying, measuring, monitoring, and controlling risks.

Any investment strategy must incorporate risk management. The objective of risk management is to reduce the probability of loss and maximize the expected return on investments.

These are the core elements of risk management

-

Identifying risk sources

-

Measuring and monitoring the risk

-

How to control the risk

-

How to manage the risk

What is a Financial Planner? How can they help with wealth management?

A financial planner is someone who can help you create a financial plan. They can evaluate your current financial situation, identify weak areas, and suggest ways to improve.

Financial planners are trained professionals who can help you develop a sound financial plan. They can advise you on how much you need to save each month, which investments will give you the highest returns, and whether it makes sense to borrow against your home equity.

Most financial planners receive a fee based upon the value of their advice. However, some planners offer free services to clients who meet certain criteria.

What is wealth management?

Wealth Management involves the practice of managing money on behalf of individuals, families, or businesses. It covers all aspects related to financial planning including insurance, taxes, estate planning and retirement planning.

Who Should Use a Wealth Manager?

Anyone who is looking to build wealth needs to be aware of the potential risks.

For those who aren't familiar with investing, the idea of risk might be confusing. Poor investment decisions can lead to financial loss.

People who are already wealthy can feel the same. They may think they have enough money in their pockets to last them a lifetime. They could end up losing everything if they don't pay attention.

Everyone must take into account their individual circumstances before making a decision about whether to hire a wealth manager.

How to choose an investment advisor

Selecting an investment advisor can be likened to choosing a financial adviser. Experience and fees are the two most important factors to consider.

An advisor's level of experience refers to how long they have been in this industry.

Fees are the price of the service. It is important to compare the costs with the potential return.

It's crucial to find a qualified advisor who is able to understand your situation and recommend a package that will work for you.

Statistics

- According to a 2017 study, the average rate of return for real estate over a roughly 150-year period was around eight percent. (fortunebuilders.com)

- As previously mentioned, according to a 2017 study, stocks were found to be a highly successful investment, with the rate of return averaging around seven percent. (fortunebuilders.com)

- Newer, fully-automated Roboadvisor platforms intended as wealth management tools for ordinary individuals often charge far less than 1% per year of AUM and come with low minimum account balances to get started. (investopedia.com)

- These rates generally reside somewhere around 1% of AUM annually, though rates usually drop as you invest more with the firm. (yahoo.com)

External Links

How To

How do I become a Wealth advisor?

A wealth advisor is a great way to start your own business in the area of financial services and investing. There are many opportunities for this profession today. It also requires a lot knowledge and skills. These qualities are necessary to get a job. A wealth advisor is responsible for giving advice to people who invest their money and make investment decisions based on this advice.

The right training course is essential to become a wealth advisor. It should cover subjects such as personal finances, tax law, investments and legal aspects of investment management. After completing the course, you will be eligible to apply for a license as a wealth advisor.

Here are some suggestions on how you can become a wealth manager:

-

First, it is important to understand what a wealth advisor does.

-

It is important to be familiar with all laws relating to the securities market.

-

You should study the basics of accounting and taxes.

-

After you complete your education, take practice tests and pass exams.

-

Final, register on the official website for the state in which you reside.

-

Apply for a work permit

-

Take a business card with you and give it to your clients.

-

Start working!

Wealth advisors usually earn between $40k-$60k per year.

The size of the business and the location will determine the salary. So, if you want to increase your income, you should find the best firm according to your qualifications and experience.

We can conclude that wealth advisors play a significant role in the economy. Everyone should be aware of their rights. You should also be able to prevent fraud and other illegal acts.